Sasin Insights with Assistant Professor Chonawee Supatgiat

26 October 2022

Case Studies: Covid- 19 Insurance Policy Failure and Risk Diversification

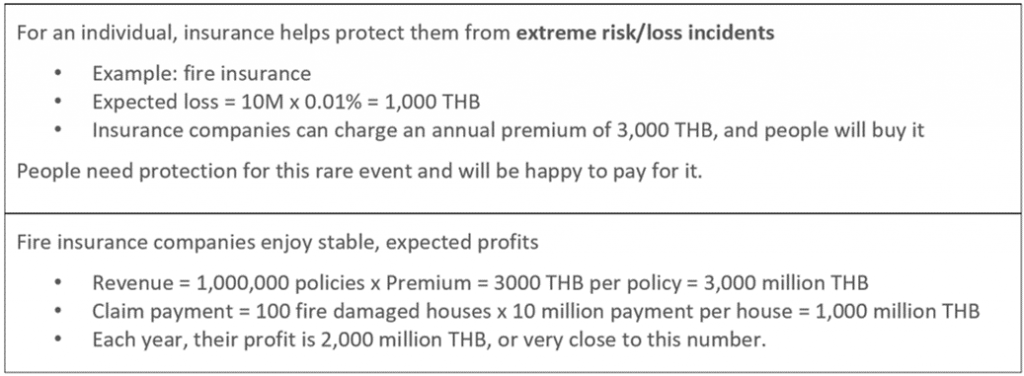

Unwittingly, insurance companies in Thailand offered cheap 500 Baht ($19) Covid-19 insurance policies in 2020, where policyholders will get 100,000 Baht ($2,758) if they get infected with the disease. In 2021, Nikkei Asia reported that the insurance policy resulted in the profit loss of sixteen Thai insurance companies. Ten insurance companies reported a loss of 5.8 billion baht ($176 million), and four insurance companies went bankrupt. Chonawee Supatgiat, Ph.D., Assistant Professor in Finance, Sasin School of Management, said that the failure of the Covid-19 insurance policy resulted from a lack of risk diversification in their policies. In general, insurance protects policyholders from extreme losses like fire insurance. “In the case of a fire, policyholders need to pay only 1000 Baht ($28), not 10 million Baht ($277,085) for repairment of their houses. The insurance company can also charge the annual premium price of 3,000 Baht ($83) [for the insurance], and people will be happy to buy it,” he said, adding that this is the rule of large numbers that come to play in risk diversification. Table 1.1: Fire Insurance Risk Diversification

“Fire insurance companies enjoy a stable expected profit of 2,000 million baht since the revenue comes from the number of policies they have, “ he explained.

“With Covid-19, we cannot diversify the government risk as we have only one government, so it cannot be diversified- Covid-19 insurance is just a gamble bet on a single risk event.” – Chonawee Supatgiat, Ph.D.

An insurance company may have 1 million policies, so its revenue will be: 1,000,000 policies x Premium insurance price = 3000 Baht per policy. Their total revenue will be 3,000 million Baht. With the claim payment, supposing that there were 100 fire-damaged houses (each year), this can be multiplied by 10 million Baht payment per house, which amounts to 1,000 million Baht. The fire insurance company enjoys 2,000 million Baht each year. (See Table 1.1)

“The beauty of the insurance business is that it is a win-win deal. The policyholder no longer had to face extreme risks while the company makes a good stable profit,” Assistant Professor Chonawee said.

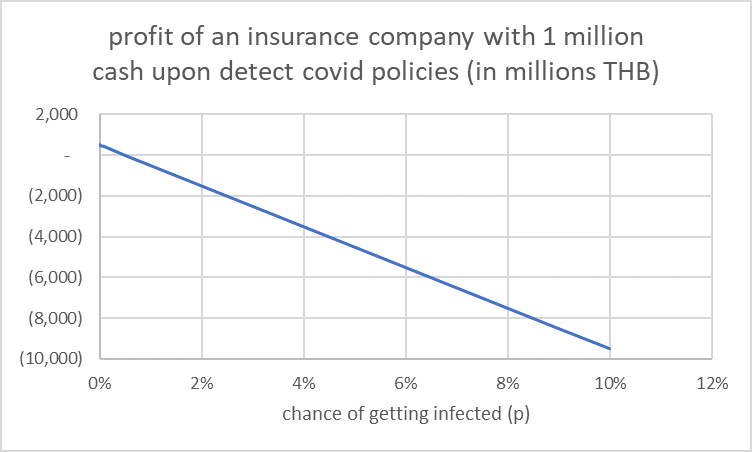

In the case of the cash upon detection Covid policy, however, there is no risk diversification, resulting in profit losses and bankruptcy. “In the fire insurance case, we have the strong law of large numbers that can diversify risks because there are one million houses,” he said, “With Covid-19, we cannot diversify the government risk as we have only one government, so it cannot be diversified- Covid insurance is just a gamble bet on a single risk event.”

In other words, Covid failure was dependent on only one factor, the government movement control policy, relying on their decision on whether they will decide if they will lock down the country.

Table 1.1: Fire Insurance Risk Diversification

“Fire insurance companies enjoy a stable expected profit of 2,000 million baht since the revenue comes from the number of policies they have, “ he explained.

“With Covid-19, we cannot diversify the government risk as we have only one government, so it cannot be diversified- Covid-19 insurance is just a gamble bet on a single risk event.” – Chonawee Supatgiat, Ph.D.

An insurance company may have 1 million policies, so its revenue will be: 1,000,000 policies x Premium insurance price = 3000 Baht per policy. Their total revenue will be 3,000 million Baht. With the claim payment, supposing that there were 100 fire-damaged houses (each year), this can be multiplied by 10 million Baht payment per house, which amounts to 1,000 million Baht. The fire insurance company enjoys 2,000 million Baht each year. (See Table 1.1)

“The beauty of the insurance business is that it is a win-win deal. The policyholder no longer had to face extreme risks while the company makes a good stable profit,” Assistant Professor Chonawee said.

In the case of the cash upon detection Covid policy, however, there is no risk diversification, resulting in profit losses and bankruptcy. “In the fire insurance case, we have the strong law of large numbers that can diversify risks because there are one million houses,” he said, “With Covid-19, we cannot diversify the government risk as we have only one government, so it cannot be diversified- Covid insurance is just a gamble bet on a single risk event.”

In other words, Covid failure was dependent on only one factor, the government movement control policy, relying on their decision on whether they will decide if they will lock down the country. “If the government decides to lockdown the country, p [the possibility of a disaster occurring] can be as low as 0.01% for all people, but if the government decides on having no lockdowns, p can be high as 9% for all people,” he said. He added that the strong law of large number in the fire insurance case is inapplicable to this case because Thailand has just one government, so the risks for Covid-19 insurance are undiversifiable.

“Insurance companies should not focus on this type of risk because it cannot be diversified. They should focus on risks that can be diversified, as in the fire insurance case,” Professor Chonawee concluded.

“If the government decides to lockdown the country, p [the possibility of a disaster occurring] can be as low as 0.01% for all people, but if the government decides on having no lockdowns, p can be high as 9% for all people,” he said. He added that the strong law of large number in the fire insurance case is inapplicable to this case because Thailand has just one government, so the risks for Covid-19 insurance are undiversifiable.

“Insurance companies should not focus on this type of risk because it cannot be diversified. They should focus on risks that can be diversified, as in the fire insurance case,” Professor Chonawee concluded.

Share this article